Navigating the ever-evolving world of cryptocurrency exchanges can feel overwhelming, especially for those new to digital assets. Among the many platforms vying for attention, BitMart Exchange has steadily gained traction as a global player promising speed, security, and a broad asset selection. But as with any online exchange handling millions in user funds, critical questions arise. Can BitMart truly be trusted? Is it secure enough for both seasoned traders and crypto novices? And how does it stack up against its competitors in terms of features, compliance, and user experience?

In this comprehensive review, we dive deep into the operations, safeguards, pros, and pitfalls of BitMart Exchange to help you determine whether it’s a suitable platform for your trading goals. From security protocols and supported cryptocurrencies to customer support and regulatory transparency, we examine every aspect that matters. Whether you’re considering your first crypto purchase or looking to switch from another exchange, understanding the ins and outs of BitMart can help you make a confident and informed decision.

Overview

Mortgage rates have gone up and down over the years, depending on the economy. Right now, they are higher than usual, making borrowing more expensive.

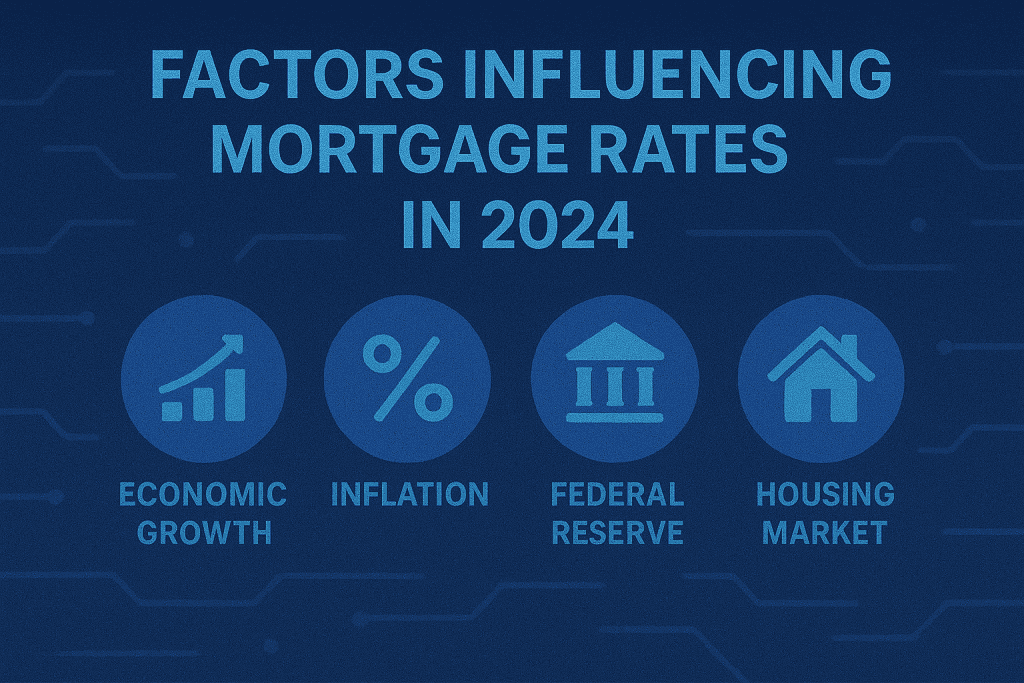

Key Factors Affecting Mortgage Rates:

- Federal Reserve decisions – The Fed raises or lowers interest rates to control inflation.

- Inflation levels – High inflation often leads to higher mortgage rates.

- Job market strength – A strong job market can keep rates higher.

- Housing demand – If many people want to buy homes, rates may stay high.

- Global economy – Events like recessions or market crashes can push rates down.

What Affects Mortgage Rates?

Why Do Mortgage Rates Change?

Mortgage rates don’t just go up and down randomly. They are influenced by several big factors, including the economy, government policies, and investor behavior. If you’re planning to buy a home or refinance, understanding these factors can help you make better decisions.

1. The Federal Reserve and Interest Rates

The Federal Reserve (the Fed) plays a huge role in mortgage rates. When inflation is high, the Fed raises interest rates to slow down spending. This makes borrowing more expensive, which includes mortgages. On the other hand, when the economy is struggling, the Fed lowers interest rates to encourage borrowing and investment.

For example, during the COVID-19 pandemic, the Fed dropped interest rates to historic lows to stimulate the economy. As a result, mortgage rates fell, making it a great time to buy a home. But in 2022 and 2023, inflation surged, and the Fed had to increase rates. That’s why mortgage rates went up.

2. Inflation and Mortgage Rates

Inflation is another key factor. When the cost of goods and services rises, lenders adjust mortgage rates to keep up. High inflation usually leads to higher mortgage rates because lenders want to make sure they still earn a profit after inflation eats away at the value of money.

In simple terms:

- If inflation is high → Mortgage rates go up.

- If inflation is low → Mortgage rates may go down.

3. The Housing Market and Demand

Mortgage rates are also affected by supply and demand in the housing market. If there are more buyers than available homes, home prices rise, and mortgage rates tend to stay high. But if fewer people are buying homes, lenders may lower rates to attract borrowers.

Right now, home prices are still high in many areas because there aren’t enough houses available. This keeps mortgage rates from dropping quickly, even when other factors suggest they should.

4. Investor Confidence and the Financial Market

Investors don’t just put their money into real estate. They also invest in stocks, bonds, and even the crypto market. If investors feel uncertain about the stock market or bitcoin and blockchain investments, they might move their money into safer assets, like mortgage-backed securities (MBS).

When investors put more money into MBS, mortgage rates tend to drop. But if they pull money out of MBS and invest in riskier assets, mortgage rates may rise.

5. The Job Market and Economy

A strong job market means more people can afford homes, which increases demand for mortgages. If unemployment is low and wages are rising, mortgage rates may stay high because lenders know borrowers can handle higher payments. But if the job market weakens and people start losing jobs, mortgage rates might drop to encourage more home buying.

Will Mortgage Rates Go Down Soon?

Mortgage rates will only drop when inflation slows, the Fed lowers interest rates, and housing demand balances out. Many experts believe rates could start to decrease in late 2024, but it all depends on how these factors play out. If you’re thinking about buying a home, keeping an eye on these trends can help you decide when the right time is to lock in a mortgage.

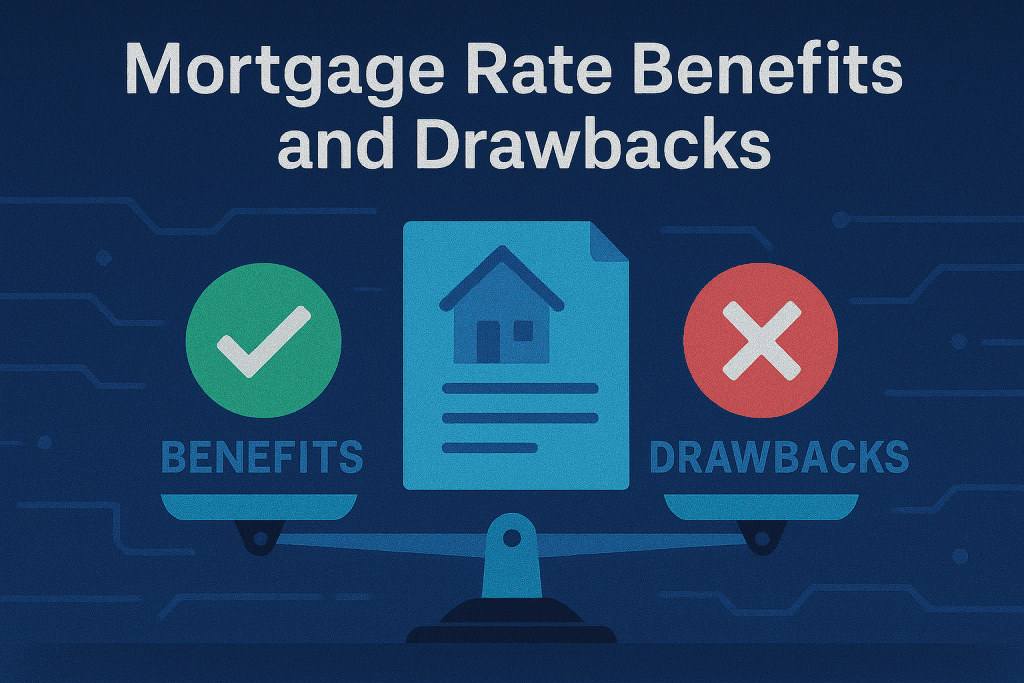

Pros and Cons of Current Mortgage Rates

Mortgage rates being high has both upsides and downsides. Let’s break it down:

| Pros | Cons |

|---|---|

| If rates drop later, homeowners can refinance at a lower rate. | High rates make home loans more expensive. |

| High rates may slow home price growth, making homes more affordable. | Monthly payments for new buyers are higher. |

| Buyers with cash offers have an advantage over those using loans. | Fewer people can qualify for home loans. |

When Will Mortgage Rates Go Down: Current Rates

Mortgage rates vary based on factors like credit score and loan type. Here’s a look at current rates:

| Loan Type | Current Average Rate |

|---|---|

| 30-Year Fixed | 6.5% – 7.0% |

| 15-Year Fixed | 5.8% – 6.2% |

| 5/1 Adjustable | 6.0% – 6.5% |

Some experts predict that if inflation drops, mortgage rates could decrease by late 2024 or early 2025. But this depends on how the economy performs.

Why Mortgage Rates Are High Right Now

Mortgage rates are high because inflation has been rising. The Fed raised interest rates to slow inflation, which made borrowing more expensive. High mortgage rates also discourage people from buying homes, which slows down the housing market.

Will Mortgage Rates Drop Soon?

It depends. If inflation slows and the economy weakens, the Fed might lower interest rates. But if inflation stays high, rates could remain elevated. Experts believe rates might start dropping in late 2024.

How Mortgage Rates Compare to Other Investments

Mortgage rates affect real estate investments. Let’s compare real estate to other investments like bitcoin and exchange markets.

| Investment Option | Potential ROI | Risk Level |

|---|---|---|

| Real Estate | 5%-8% annually | Moderate |

| Crypto (Bitcoin) | Varies (high volatility) | High |

| Stocks | 7%-10% annually | Moderate |

While crypto and stocks offer higher potential returns, real estate remains a stable long-term investment.

Should You Buy a Home Now or Wait?

Making the Right Choice in a High-Rate Market. Many homebuyers wonder if they should wait for lower rates. Here’s what to consider:

- If you need a home now, it might be worth buying, as home prices could keep rising.

- If you can wait, lower rates might make homes more affordable later.

- If you buy now, refinancing later could save money when rates drop.

Expert Ratings on Mortgage Rate Trends

Experts have different opinions on where mortgage rates are headed:

- Federal Reserve Forecast: ★★★☆☆ (3/5) – Rates might drop, but it depends on inflation.

- Real Estate Analysts: ★★★★☆ (4/5) – Possible rate drops by late 2024.

- Investor Sentiment: ★★★☆☆ (3/5) – Uncertainty remains due to market fluctuations.

FAQ

When will mortgage rates go down?

Experts predict that rates might drop in late 2024, depending on inflation and the Fed’s decisions. If inflation slows down, rates could decrease sooner.

How does the crypto market impact mortgage rates?

The crypto market affects investor confidence. If bitcoin and blockchain investments are unstable, investors may move money into real estate, influencing mortgage rates.

Is it better to buy a home now or wait?

It depends on your financial situation. If you can afford it now, buying could be a good move. But if you can wait, you might get a lower rate in the future.

Resources

- FXEmpire BitMart Exchange Review

- Coin Bureau BitMart Review

- YouTube BitMart Review Video

- WellCrypto BitMart Broker Overview