A few years ago, a customer emailed me asking, “Do you accept crypto?” I almost ignored it. At the time, accepting Crypto Payments sounded complicated, technical, and honestly a little risky. But curiosity got the better of me. I started researching how businesses were using Cryptocurrency to attract new customers, reduce fees, and speed up transactions.

What I found surprised me.

Accepting Crypto Payments isn’t just for tech startups or global corporations. Small shops, freelancers, online creators, and service providers are using Cryptocurrency to open doors to international buyers and modern payment options. With the steady growth of the Crypto Market, customers increasingly expect flexible ways to pay.

If you’re a business owner, creator, or industry professional, learning how to accept Crypto Payments can help you reduce transaction costs, avoid chargebacks, and appeal to a tech-savvy audience. In this guide, I’ll walk you through everything step by step in simple language, so you can confidently accept Cryptocurrency and grow your business.

Tools Needed

Before you jump in, you’ll need a few basic tools. The good news? Most of them are easy to set up and don’t require technical expertise.

First, you’ll need a cryptocurrency wallet. This is where your digital assets will be stored. Then, you’ll need a payment gateway if you want to accept payments on your website. You’ll also need a business bank account if you plan to convert crypto into local currency. Finally, a secure internet connection and basic understanding of Cryptocurrency transactions are essential.

| Tool/Material | Purpose |

|---|---|

| Crypto Wallet | Stores received Cryptocurrency securely |

| Payment Gateway | Processes Crypto Payments online |

| Business Website | Allows customers to pay digitally |

| Exchange Account | Converts crypto to fiat currency |

| Secure Internet | Ensures safe transactions |

Having these tools in place makes accepting Crypto Payments smooth and manageable.

Crypto Payments Instructions

Step 1: Choose the Right Cryptocurrency

Start by deciding which digital currencies you want to accept. Many businesses begin with Bitcoin, as it’s widely recognized and trusted. Some also accept Ethereum or stablecoins to minimize price volatility.

Research your customer base. Are they active in the Coin Market? Do they prefer certain coins? Keep it simple at first. You can always expand later.

If you’re unsure, begin with one or two major options. That keeps accounting easier and helps you test the waters without overwhelming yourself.

Step 2: Set Up a Crypto Wallet

Next, create a secure wallet. Think of it as your digital cash register for Crypto Payments.

There are custodial wallets (managed by third parties) and non-custodial wallets (where you control the private keys). If you’re new, a reputable custodial wallet might feel easier. If security and control are your priority, consider a hardware wallet.

Write down your recovery phrase and store it somewhere safe. Not in your email. Not on your phone. I learned this the hard way when I nearly lost access during my first setup.

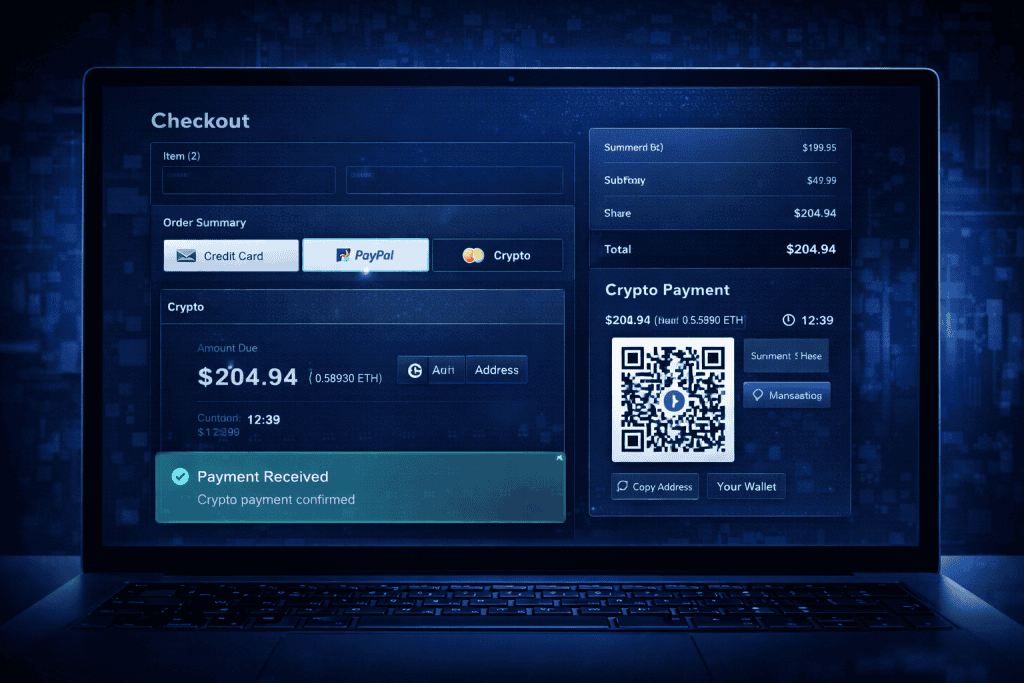

Step 3: Choose a Payment Gateway

If you run an online business, a crypto payment gateway simplifies everything. It integrates with your checkout page and automatically processes Crypto Payments.

Many gateways offer automatic conversion into local currency, which protects you from price swings. This can be helpful if you’re worried about volatility.

Look for transparent fees, security features, and compatibility with your website platform. Some popular providers are highlighted in the resources section below.

Step 4: Integrate Crypto Payments Into Your Website

Once you’ve chosen your gateway, connect it to your site. Most platforms like Shopify or WooCommerce offer simple plugins.

Test the system before announcing it publicly. Make a small transaction yourself to ensure everything works smoothly. It takes a few minutes but saves you from embarrassing checkout issues.

Clear communication is key. Add a “We Accept Crypto Payments” badge on your homepage or checkout page. Customers appreciate clarity.

Step 5: Update Accounting and Tax Records

Here’s the part many people overlook.

Every Cryptocurrency transaction needs proper documentation. Depending on your country, crypto may be treated as property or income.

Speak with an accountant familiar with Blockchain transactions. Keep records of transaction values at the time of payment. This protects you during tax season and ensures your new Investment in crypto acceptance remains compliant.

Crypto Payments Tips and Warnings

Accepting Crypto Payments can be exciting, but it’s important to approach it wisely.

First, understand price volatility. Cryptocurrency values can fluctuate dramatically. If you prefer stability, enable automatic conversion into fiat currency.

Second, educate your staff. Even a basic understanding prevents confusion. Make sure everyone knows how to confirm a transaction before delivering goods or services.

Third, be transparent about refunds. Since crypto transactions are irreversible, outline a clear refund policy.

Here are some practical reminders:

| Tip or Warning | Why It Matters |

|---|---|

| Enable Auto-Conversion | Reduces exposure to price swings |

| Double-Check Wallet Address | Prevents irreversible errors |

| Train Staff | Ensures smooth processing |

| Keep Detailed Records | Helps with taxes and compliance |

| Start Small | Minimizes risk while learning |

One mistake I’ve seen is businesses jumping in without understanding transaction confirmations. Always wait for confirmations before finalizing orders.

Also, stay updated with Cryptocurrency regulations in your region. Rules can change.

When done correctly, accepting Crypto Payments can lower fees compared to credit cards and eliminate chargebacks. But like any financial tool, it requires responsibility.

Conclusion

Accepting Crypto Payments may seem intimidating at first, but once you break it down, it’s surprisingly manageable. Choose your preferred coins, set up a secure wallet, integrate a payment gateway, test your system, and keep accurate records.

That’s it.

Cryptocurrency is no longer a niche experiment. It’s becoming part of everyday commerce. By adding Crypto Payments to your checkout options, you open your business to global customers and modern financial tools.

Start small. Test one transaction. Learn as you go.

You might be surprised how quickly customers respond positively when they see you accept Cryptocurrency. The future of payments is evolving, and now you’re ready to be part of it.

FAQ

How do small businesses start accepting Crypto Payments in the Cryptocurrency industry?

Small businesses can begin by setting up a digital wallet and partnering with a reliable crypto payment gateway. Many platforms make it easy to integrate Crypto Payments into existing websites. Start with major currencies, test transactions, and consult an accountant familiar with Cryptocurrency tax regulations to ensure compliance.

Are Crypto Payments safe for online businesses in the Cryptocurrency market?

Yes, Crypto Payments are generally secure because they operate on Blockchain technology, which records transactions transparently and permanently. However, businesses must protect private keys, verify wallet addresses carefully, and use reputable gateways. Security depends on proper setup and responsible management.

What are the benefits of accepting Crypto Payments for global customers in the Cryptocurrency space?

Accepting Crypto Payments allows businesses to reach international customers without traditional banking delays or high fees. Transactions are often faster and reduce chargeback risks. For companies targeting digital audiences in the Cryptocurrency sector, it also strengthens brand credibility and innovation appeal.

Resources

- Coinpaper. How to Accept Crypto Payments as a Business (2024 Guide)

- Forbes Advisor. How to Accept Bitcoin at Your Business

- BVNK. How to Accept Crypto as a Business

- Fit Small Business. How to Accept Crypto as a Business

- CoinGape. Best Cryptocurrency Payment Gateway