Introduction

Central bank digital currencies (CBDCs) are rapidly emerging as a force for change in the global financial landscape. As we move into 2024, their potential to revolutionize digital payments and enhance financial inclusion is becoming increasingly clear. In this review, we take a closer look at the complexities of central bank digital currencies (CBDCs) and explore their role in reshaping the way money is used, stored, and transferred. By understanding the benefits and challenges associated with CBDCs, you can better understand why they are garnering so much interest from governments, financial institutions, and consumers alike.

Overview

A CBDC is a digital currency issued and regulated by a country’s central bank. Unlike cryptocurrencies, they are pegged to the value of a country’s currency, offering the stability of traditional fiat currencies and the efficiency of digital transactions. Interest in CBDCs is growing because of their potential to improve financial access, streamline payment processes, and increase the security of transactions. In regions that lack banking infrastructure, such as the Middle East, CBDCs could potentially bridge the gap and bring more people into the financial system.

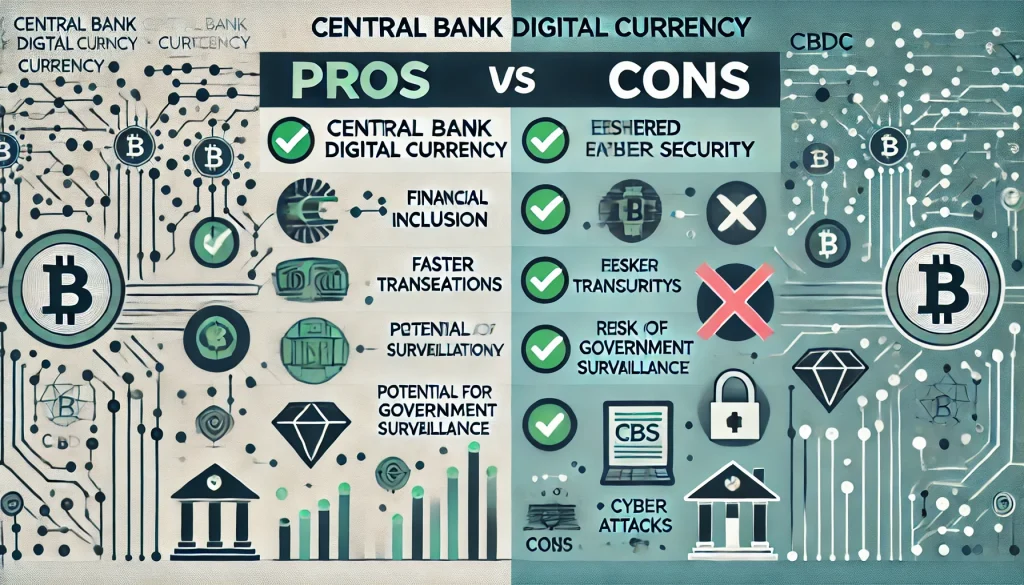

Pros and cons

Pros

- Financial inclusion: CBDCs can significantly improve access to financial services, especially in underbanked areas, providing a secure and accessible platform for digital transactions.

- Payment efficiency: Reduce transaction costs and time by eliminating intermediaries and enable real-time payments domestically and internationally.

- Regulatory oversight: CBDCs are controlled by central banks, ensuring regulatory compliance and reducing the risk of fraud or illegal activity.

Cons

- Privacy concerns: Due to the centralized nature of CBDCs, transactions can be monitored by authorities, which can raise privacy concerns among users.

- Implementation costs: Developing and maintaining a CBDC infrastructure is expensive and requires significant investment in technology and cybersecurity.

- Potential disruption: The introduction of CBDCs could disrupt the existing banking system, causing economic and financial hardship during the transition period.

Deep dive analytics

Design

CBDCs are designed to seamlessly integrate with existing financial systems while providing enhanced digital capabilities. They are issued as digital currencies that are equivalent to national currencies and can be stored in digital wallets provided by central banks or authorized financial institutions. They are designed with security as a top priority, using advanced cryptography to protect transactions.

Features

The function of a CBDC is centered on providing fast, reliable, and cost-effective payment solutions. By utilizing blockchain technology, CBDCs can facilitate the instant settlement of transactions, reducing the need for intermediaries. This efficiency is particularly useful for cross-border transactions, which are traditionally slow and costly.

Security

Security is an important aspect of CBDCs. However, central banks around the world are investing heavily in cybersecurity measures to protect the integrity of CBDCs, as their digital nature makes them vulnerable to cyber threats. The use of blockchain technology also adds an extra layer of security, as transactions are immutable and traceable.

Monetary policy implications

CBDCs provide central banks with a more accurate tool to implement monetary policy. It allows for direct control of the money supply and more accurate data collection on economic activity, which can lead to more effective policy interventions, especially during economic crises.

Compare

Compared to traditional payment systems like credit cards or bank transfers, CBDCs have several advantages. They cut out the need for intermediaries, which reduces transaction costs and speeds up payment processing. Unlike cryptocurrencies like Bitcoin, CBDCs are backed by central bank reserves, making them more stable. However, unlike decentralized cryptocurrencies, CBDCs are regulated by governments, which can be a turn-off for users who value financial privacy and autonomy.

Compare payment systems

| Features | CBDCs | Cryptocurrency (e.g., Bitcoin) | Existing payment systems (such as credit cards) |

|---|---|---|---|

| Regulation | Central bank regulation | Decentralized, unregulated | Regulation of financial institutions |

| Transaction speed | Immediate | Variety | Generally slow |

| Security | High, government support | High but vulnerable to fraud | High, security measures are in place |

| Stability | Stable, national currency support | Volatility | Stable |

Conclusion

Central bank digital currencies represent an important leap forward in the evolution of money. They offer a range of benefits, including financial inclusion and greater payment efficiency, but they also come with challenges, including privacy concerns and high implementation costs. As countries continue to explore and implement digital currencies, their success will depend on balancing innovation and regulation.

Evaluation

4/5 – CBDCs are a promising innovation, but they need to overcome several hurdles before they can be widely adopted.

FAQ

What is a central bank digital currency (CBDC)?

A central bank digital currency is a digital currency issued by a central bank that serves as the digital equivalent of a country’s fiat currency.

How do CBDCs improve financial inclusion?

CBDCs provide access to financial services in areas with limited existing banking infrastructure, enabling secure digital transactions.

Are CBDCs the same as cryptocurrencies?

No, unlike cryptocurrencies, CBDCs are regulated by a central bank and are pegged to the value of a national currency to ensure stability.

See also

- International Monetary Fund. (2024, June 18). Central bank digital currencies can boost Middle East’s financial inclusion, payment efficiency. IMF. https://www.imf.org/en/Blogs/Articles/2024/06/18/central-bank-digital-currencies-can-boost-middle-easts-financial-inclusion-payment-efficiency

- Afshari, A., & Mohammadkhani, A. (2024). The role of central bank digital currencies (CBDCs) in financial inclusion: Evidence from developing economies. SHS Web of Conferences, 151, 02007. https://www.shs-conferences.org/articles/shsconf/abs/2024/01/shsconf_icdeba2023_02007/shsconf_icdeba2023_02007.html

- Atlantic Council. (2024). Central bank digital currency (CBDC) tracker. https://www.atlanticcouncil.org/cbdctracker/

- Park, H., & Kim, J. (2024). Impacts of central bank digital currencies on global financial markets. International Review of Financial Analysis, 84, 102547. https://www.sciencedirect.com/science/article/pii/S1057521923005471

- Li, Y., & Zhang, X. (2024). The future of digital currencies: A comparative study of CBDCs and cryptocurrencies. Asian Journal of Business, 15(1), 32-45. https://www.emerald.com/insight/content/doi/10.1108/AJB-12-2023-0210/full/html